Key Points

- The CEO and CFO of Nvidia are just like any other investor because they own a large amount of shares in the company.

- An industry CEO predicts a data centre AI chip market that would expand at a CAGR of approximately 73% through 2027, and the company is the undisputed leader in this space.

- It will be difficult for rivals to gain market share from Nvidia because of the large moat surrounding its graphics processing units (GPUs) that enable artificial intelligence (AI).

In celebration of the 25th anniversary of the leading AI chip manufacturer’s public offering, we present 25 compelling arguments in favour of purchasing shares in the company.

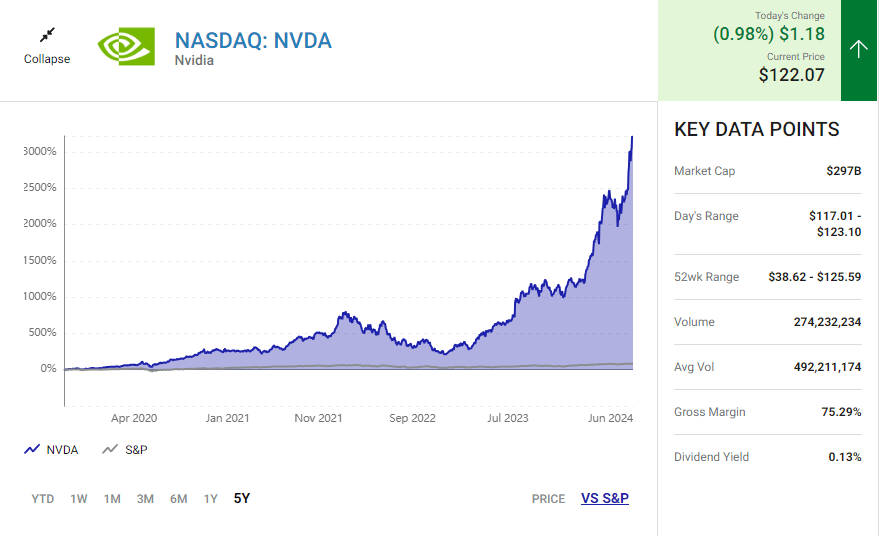

This Nvidia Stock (NVDA 0.98%) has been an outstanding performer both in the short term and over the long term. In January of 1999, six years after the company was established, the artificial intelligence (AI) chip industry leader was able to successfully complete its first public offering (IPO). As a way to celebrate the fact that Nvidia Stock turned 25 years old earlier this year, the following list of 25 reasons to purchase it is presented in no particular order.

Although increasing the amount of cash that is returned to shareholders and making NVDA stock more “accessible” are examples of what Wall Street would refer to as positive catalysts, they are not sufficient reasons in and of themselves to commit extra capital to any company at any level. NVDA stock is less accessible than other stocks.

For some context, Nvidia operates in four different market platforms: the data centre, gaming, professional visualisation, and the automotive and robotics industries. The data centre is the company’s most important business (it accounted for 87 percent of sales in the most recent quarter) and is experiencing the most rapid expansion as a result of the increasing usage of artificial intelligence, particularly generative AI. With the launch of the ChatGPT chatbot in the latter half of 2022, generative artificial intelligence (AI) stormed onto the scene.

Why Nvidia Stock is a Smart Investment

1.The founder heads the company

Of the three co-founders of Nvidia, Jensen Huang was one of the first employees. Over the long run, research shows that stocks of companies led by founders do better than other types of companies.

2.The founder-CEO is highly invested

Based on the most recent data that is available, Huang is the owner of about 868 million shares of Nvidia stock as a result of the 10-for-1 stock split that took place on Friday (which was detailed in No. 6). As of the stock’s closing price on June 7, this holding is estimated to be worth around 105 billion dollars. With such a substantial investment, investors may feel assured that Huang’s objectives are congruent with their own.

3.Nvidia’s future appears to be bright, according to the CFO’s massive Nvidia Stock holdings

After the 10-for-1 Nvidia Stock split that took place on Friday (which was detailed in No. 6), Chief Financial Officer Colette Kress now controls 6.43 million shares of Nvidia Stock. As of June 7, the value of these shares was about 777 million dollars. There is a good chance that a Chief Financial Officer (CFO) has the best understanding of the firm’s financial performance at any given time, even more so than the CEO of the company. In light of this, it is reasonable to assert that Kress is quite bullish regarding the growth possibilities of Nvidia Stock.

4. Over the long run, Nvidia stock has been really amazing

Up to June 7, the Nvidia Stock has returned 25,431% over the course of the previous ten years. That is more than one hundred times the return of 230% that the S&P 500 index brings in. An investment of one thousand dollars in Nvidia stock ten years ago would today be worth more than two hundred and fifty thousand dollars.

The success of a Nvidia Stock in the past does not always ensure that it will do well in the future. On the other hand, the long-term performance of Nvidia Stock frequently reflects the capacity of a company’s senior management to devise and carry out initiatives that are effective.

For more content, visit: https://iqresearcher.com

5. AI market is expected to maintain its rapid growth

According to Statista, the worldwide artificial intelligence market is anticipated to achieve a revenue of $184 billion in 2024. Furthermore, it is anticipated to have a compound annual growth rate (CAGR) of 28.5% until the year 2030, when it is anticipated to be worth an estimated $826.7 billion.

For Nvidia Stock, whose graphics processing unit (GPU) chips and other associated goods and services are utilised for the purpose of training and deploying artificial intelligence systems, this is a hugely welcome development..

6. The 10-for-1 Nvidia Stock splitation took place on June 7th

In the morning of Friday, June 7, Nvidia stock was divided ten to one. The shareholders who had ownership of the stock as of the previous day were given nine more shares for every share that they had previously possessed. Monday, June 10 is the day when the stock is planned to resume trading on a basis that takes into account the split.

Nvidia shares reached a closing price of $1,208.88 on Friday, which indicates that its split-adjusted price was $120.89 at the time of settlement.

An increase in price as a result of increased demand for shares and an increased likelihood of being included on the Dow Jones Industrial Average index are two potential advantages that investors may stand to gain from the Nvidia Stock split that Nvidia has implemented.

7. The data centre AI chip market is dominated by the business

It is generally believed that Nvidia holds more than 90 percent of the market for artificial intelligence graphics processing unit (GPU) chips for data centres, and that it holds more than 80 percent of the market for AI chips for data centres overall.

8. According to projections, the data centre AI chip industry will keep expanding at a phenomenal rate

According to an estimate made by Lisa Su, CEO of Advanced Micro Devices (AMD -4.39%), the worldwide market for chips that speed artificial intelligence processing in data centres was estimated to be worth around $45 billion in the year 2023. She forecasts that by the year 2027, this sector would generate revenue of $400 billion, which is equivalent to a staggering compound annual growth rate of 72.7%.

9. A number of benefits give Nvidia’s data centre division a leg up in the market

Nvidia’s territory, which consists of GPUs for data centres that enable artificial intelligence, has lately been invaded by Advanced Micro Devices (AMD) and Intel. There is no need for investors to be excessively alarmed. Not only does Nvidia’s graphics processing units (GPUs) contribute to the company’s competitive advantages, but so does its software, in particular CUDA, which has been utilised by millions of developers for a considerable amount of time. CUDA makes it possible for graphics processing units (GPUs) to have the parallel processing capabilities that are necessary for boosting general and artificial intelligence computing.

10. Its income is increasing at Nvidia Stock

Over the course of the past four quarters, beginning with the most recent quarter, Nvidia Stockhas had year-over-year revenue growth of 262%, 265%, 206%, and 101% with each quarter.

11. The rate of increase in its profits is outpacing that of its revenue

The increasing profit margins of Nvidia Stock are reflected in the company’s adjusted earnings per share (EPS), which are growing at a faster rate than the company’s revenue. The company’s highly profitable data centre operation is expanding at a quicker rate than its other companies, which is the driving force behind this dynamic. Over the course of the past four quarters, beginning with the most current quarter, the following is the year-over-year adjusted earnings per share increase of the company: 461 percent, 486 percent, 593 percent, and 429 percent.

12. Its FCF is likewise expanding at a quick pace

Over the course of the past four quarters, beginning with the most recent quarter, Nvidia has had a year-over-year rise in its free cash flow (FCF) of 465%, 546%, N/A (FCF was negative in the period from the previous year), and 634%.

13. The financial markets anticipate robust profit growth in the coming five years

Nvidia is expected to expand its adjusted earnings per share at an average annual rate of 46.5% over the next five years, according to projections made by Wall Street as of June 7.

14. Almost without fail, Nvidia exceeds the expectations of Wall Street

The quarterly profit predictions provided by Wall Street are almost always exceeded by Nvidia, and sometimes by a significant margin. Over the course of the last four quarters, the adjusted earnings per share of the firm have been higher than the average expectation of the analysts by percentages ranging from 10% to 29%.

Nvidia’s compound annual growth rate (CAGR) over the next five years will be greater than the 46.5% that experts now anticipate it would be if this trend persists..

15. The stock is being valued at a fair price

The price of Nvidia stock currently stands at 44.6 times the company’s forward expected profits as of Friday’s closing price. This is a high valuation when considered in isolation. Wall Street anticipates that the firm will grow adjusted earnings per share by 109% during the current fiscal year and at an average annual rate of 46.5% over the following five years. This is a fair expectation for the company. According to the information shown above, experts are probably underestimating the potential for its growth.

16. It’s much more profitable than its main competitors and peers

| Company | GAAP Profit Margin (TTM) |

| Nvidia | 53.4% |

| Advanced Micro Devices | 4.9% |

| Intel | 7.4% |

| Qualcomm | 23% |

| Broadcom | 29.9% |

17. Reportedly, it is establishing a specialised division for bespoke chips

For the purpose of capturing a portion of the custom chip development work for large technology firms that is now being performed by chipmakers such as Broadcom, Nvidia is reportedly in the process of establishing a custom chip business unit, as indicated by several sources and indications. Reportedly, the new company would assist businesses in the construction of bespoke chips for artificial intelligence and other applications.

For more content, visit: https://iqresearcher.com

18. When it comes to gaming graphics cards, it’s by far the biggest supplier

According to Nvidia’s most recent quarterly report, gaming was the company’s second largest market platform, accounting for 10% of the company’s total revenue. This business is the most significant provider of graphics cards for use in computer gaming in the whole world. As of the first quarter of 2024, Jon Peddie Research said that it has an 88% share of the market for discrete graphics processing units (GPUs) for desktop computers. Both AMD and Intel had a share of less than 1%, with AMD having a little over 12%.

19. It is anticipated that the PC gaming industry would maintain its robust expansion

According to Statista, the global market for personal computer (PC) gaming earned around $80.3 billion in revenue in 2023. The company also forecasts that this industry will be worth $141.9 billion in 2028. This is equivalent to a compound annual growth rate of around 12.1%.

20. Some of Nvidia’s revenue comes from repeat customers

The introduction of software and service products that produce recurring income is something that Nvidia has only lately started out with. According to the Chief Financial Officer Kress, the company’s software and services products hit an annualised revenue run rate of one billion dollars in the fourth quarter of the fiscal year.

21. The legalisation of autonomous vehicles is expected to significantly increase its income

When autonomous vehicles are made legal in the United States and throughout the world, Nvidia’s income is expected to get a significant boost. The DRIVE platform, which is the company’s artificial intelligence computing platform for autonomous vehicles, is being developed by hundreds of car manufacturers, tier 1 suppliers, and other companies.

In the event that Nvidia’s partners decide to implement its DRIVE platform in production cars, they are need to purchase a DRIVE AI computer for each vehicle. Mercedes-Benz, a manufacturer of premium automobiles, and BYD, a behemoth in the electric vehicle (EV) industry, are among its notable partners..

22. Its artificial intelligence (AI) division might be worth billions of dollars

In recent years, nations and other sovereign organisations have started utilising the technology developed by Nvidia in order to construct their very own autonomous artificial intelligence cloud services. In November of last year, Chief Financial Officer Kress stated that the “sovereign AI infrastructure market represents a multibillion-dollar opportunity over the next few years” during the company’s earnings call for the third quarter of fiscal year 2024.

23. Its robotics ambitions have recently been intensified

Nvidia provided significant enhancements to its Isaac robotics platform in addition to presenting its Project GR00T (Generalist Robot 00 Technology) artificial intelligence base model for humanoid robots in the month of March.

24. The company’s financials are looking well

The amount of cash and cash equivalents that Nvidia had at the end of the most recent quarter was $7.6 billion, while the company’s long-term debt was $8.5 billion.

For more content, visit: https://iqresearcher.com

25. Nvidia is a great place to work for employees

workers and past workers of Nvidia have given the firm an overall rating of 4.6 stars (on a scale of 1 to 5) on the website Glassdoor.com as of the 7th of June. As there is a limited number of top-tier technological talent, it is especially crucial for businesses in the technology sector to ensure that their employees are happy with their jobs. Nvidia has the highest ranking of all the corporations that are considered to be known as “Big Tech”.

Is it a good time to put $1,000 into Nvidia Stock?

Think about this before you invest in Nvidia stock:

The Motley Fool Stock Advisor analysis team has just completed the process of determining which ten stocks they consider to be the best for investors to purchase right now… however Nvidia was not one of those companies. There is a possibility that the ten equities that were selected would generate enormous profits in the years to come Nvidia Stock.

If you were to invest $1,000 at the time of our advice, you would have $740,690! Take into consideration the fact that Nvidia was included on this list on April 15, 2005.

Now, it is important to note that the overall average return of Stock Advisor is 726%, which is a market-crushing outperformance when compared to the S&P 500’s performance of 157%. The most recent list of the top ten should not be missed.

For more , visit this link: https://www.kiplinger.com/investing/should-you-invest-in-nvidia-after-its-stock-split

{kind=link}

I don’t think the title of your article matches the content lol. Just kidding, mainly because I had some doubts after reading the article.

Thanks for sharing. I read many of your blog posts, cool, your blog is very good.

Can you be more specific about the content of your article? After reading it, I still have some doubts. Hope you can help me.